Make Embarassing Bets

A government order, a fundraising clause, a contrarian bet — that turn out to be the same lesson: how much of your company sits in someone else's hands.

Anthropic and Jurisdiction Discussion

On Friday, at 5:21pm, Anthropic got a letter. By that evening, two of the most advanced AI models on the planet were switched off for everyone.

The company that built its entire brand on safety was shut down by the government, citing safety. Fable 5 and Mythos 5 - gone for every customer worldwide, because the order banned access for any foreign national, and Anthropic decided the cleanest way to comply was to pull the plug on all of it.

It seems that the switch that controls your core feature might not be in your hands, your office, or even your country. You rent most of your stack. And some of your landlords live in jurisdictions where you don't get a vote.

This week it became closer to a board-level question, because the order didn't stop at the hardware. The US has restricted the chips behind AI before. This was the first time it reached the models themselves - the thing founders actually build on. And the calmest line in Anthropic's statement was the one that mattered most: all other models were unaffected. The risk was never the vendor. It was depending on one thing you can't replace.

The fix is:

Abstract the layer. Build your product so you can swap the model (or the rail, or the provider) in a day.

Keep a second source for anything that fails the 30-day test.

Stop confusing "it works great" with "it's safe to depend on."

It doesn’t mean avoid US tools, frontier models, or move to a bunker. The best infrastructure available still sits with a handful of providers and there's no clean way around that.

Anthropic, for what it's worth, called the whole thing a misunderstanding and is working to turn the lights back on. Maybe it gets fixed by the time you read this. That's not the part that should keep you up. The part that should is simpler

If you’re a founder, here’s the uncomfortable exercise. Go through your stack and ask one question about each piece: could I rebuild this in 30 days if it disappeared tomorrow? Anything that gets a “no” is a dependancy.

All of this was pulled from the Byblos live feed - 600+ VC firms, 27500+ newsletters, one place.

See what else came in today at byblos.digital →

SAFE, Convertible Notes, or ASA?

Before your first round closes, someone will ask which instrument you're using: a SAFE, a convertible note, or an ASA. All three do the same basic job - they let you raise money now without agreeing on a valuation yet. Instead of arguing over what the company is worth today, you take the cash and agree it converts into equity at your next priced round, usually at a discount or a capped valuation that rewards the investor for being early. Founders use them because they're fast, cheap, and don't force a valuation fight before you have the traction to win it.

That much they share. Where they differ is what you're actually on the hook for in the gap between signing and converting.

A SAFE - short for Simple Agreement for Future Equity, invented by Y Combinator - is the simplest of the three. The investor gives you money now in exchange for the right to shares later, once you raise a priced round. It's not a loan: no interest, no maturity date, no clock. Until that round comes, it sits quietly on the cap table.

A convertible note is a short-term loan that's meant to turn into equity rather than be paid back. Because it's a loan, it charges interest - around 8% is standard in the UK - and it has a maturity date, usually 12 to 24 months out. If you haven't raised a priced round by then, the investor can ask for the money back in cash. It often gets sold as the quick, founder-friendly option, but it's the one that can come due before your next round arrives to cover it. Worth knowing the timing: UK seed-to-Series-A now averages around 29 months. Sign an 18-month note and the repayment date lands roughly a year before the round meant to solve it, which leaves you negotiating from a weak spot.

An ASA - short for Advance Subscription Agreement - is the UK-specific one most founders overlook. The investor pays now for shares that get issued at your next round. Like a SAFE, it's not a loan and carries no interest or maturity, and the outcome at conversion is much the same - but it's compatible with SEIS/EIS tax relief, which makes UK angels meaningfully more likely to invest, at no extra cost to you. The one thing to check is the trigger: an ASA usually converts on a qualifying round, so read that clause or a smaller round might not convert it.

The conversion maths across all three is nearly identical when the cap binds, which is the part founders tend to obsess over and the part that matters least. What actually matters is what you're carrying between signing and converting. For a UK pre-seed raise from UK angels, the ASA is usually the right default - same result as a SAFE, plus the tax relief that helps checks get written. For US or cross-border raises, a SAFE is the cleaner choice. A convertible note makes sense mainly when an investor requires it or it's a bridge from people already set up for them - not as a default.

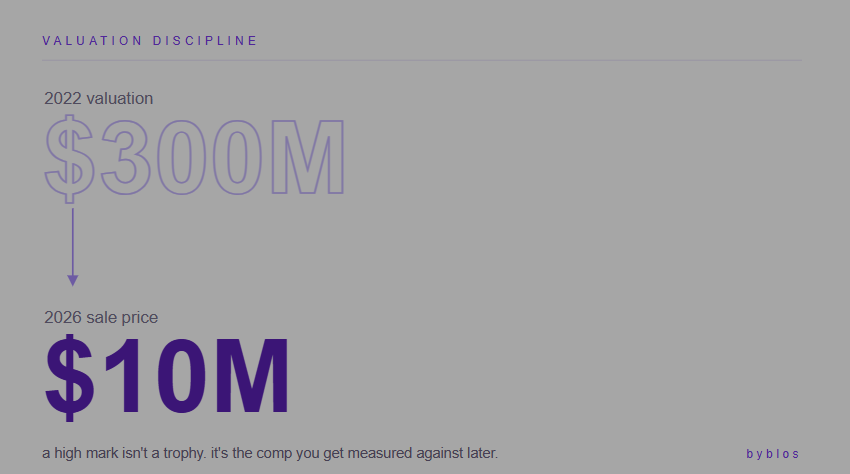

A high valuation cap feels like winning the negotiation, but it isn't a prize, it's a hurdle. It becomes the number your next round has to beat, and the comp you get measured against if it doesn't. Messari carried a $300M valuation in 2022 and sold for around $10M this year. The mark always comes due eventually, so raise at one your next round can actually clear.

Embarassing bets are the best bets

Boost VC wrote checks into crypto and "sci-fi" in 2013, when admitting you took those meetings was mildly awkward. The returns didn't come from being smart. They came from being willing to sit in the room everyone else found embarrassing. The edge was tolerance for looking a little foolish, which tends to get relabelled as conviction once it works.

The trouble in 2026 is that everyone already agrees with this. "Be contrarian" is the most consensus opinion in venture, and the same people who say it tend to back the identical AI wrapper as everyone else. Real contrarianism feels slightly dumb - the kind of thing your group chat would screenshot.

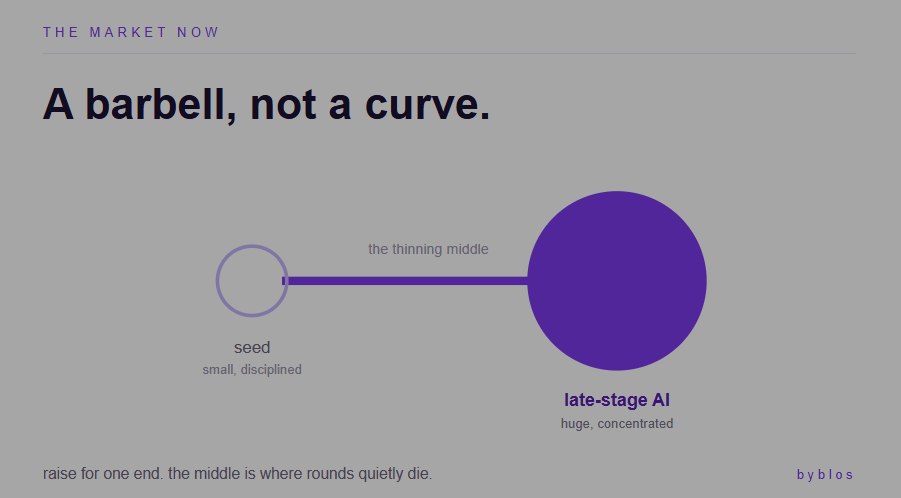

So it's worth noticing where the less obvious money is actually going. The mega-rounds this month went to physical things rather than apps: Jeff Bezos's industrial-AI startup raised a $12B round, and a German robotics company raised up to $1.4B, led by a stablecoin issuer. Energy and nuclear, dull for years, are suddenly strategic because all this AI has to plug into something. Decentralized AI was a punchline until Friday, when one government switched off a frontier model and handed the "what if no single party could do that" argument a real-world reason to exist. And tokenization keeps crowding into T-bills, the easiest thing to put on-chain, while the harder and larger opportunity sits in things like parametric insurance.

None of these are fashionable, and all of them are getting funded. That's not a coincidence, it's the mechanism. If it feels safe and obvious, you're probably early to being late instead.

In 2013 it was crypto. Right now it's robots, reactors, censorship-resistant compute, and whatever sounds faintly ridiculous this week. The useful skill is genuinely being able to sit in the embarrassing one a little longer than everyone else.

The deals worth knowing

A quick read on the week's biggest moves, and what each one actually tells a founder.

SpaceX — IPO, ~$75B raised at a $1.77T valuation. The largest IPO in history. The number isn't the point; the liquidity is. Big exits send cash back to LPs, who recommit, which eventually trickles down to early rounds — on a lag. It priced at roughly 92× sales, so read it as froth at the top, not a starting gun.

Blockworks → Messari, ~$10M. A crypto-data platform worth about $300M in 2022, sold for a sliver of that. Half cautionary tale (the mark comes due), half land grab — whoever owns the data record gets to be the thing everyone checks.

Prometheus (Bezos) — $12B Series B at a $41B valuation. Industrial AI. The mega-money is moving toward AI that runs factories, not AI that writes captions.

NEURA Robotics — up to $1.4B Series C, led by Tether. Physical AI, funded by a stablecoin issuer. Crypto money is quietly flowing into robots; atoms are the trade.

Kalshi — $1.2B Series F. Prediction markets went from "is this even legal" to a billion-dollar round in about 18 months. A category being born in real time.

Everything in today’s digest came from the Byblos live feed. The full newsletter archive, the VC directory, and tomorrow’s signal are all waiting for you at Byblos.digital - the investor interned, curated.

Our X (for timely updates and founder/investor opps)

Our Linkedin (for connections and professional insights)

Our app (for VC index cards, the feed of newsletters, and upcoming AI summaries)

That’s the data. Now go build something.