The Stablecoin Myth Got Data

McKinsey dropped the data nobody wanted. The GPU is unbundling. DeFi's composability was the contagion channel. And perps are eating every asset class.

35 newsletters from 22 VCs. The Breakdown dropped McKinsey data that challenges the stablecoin narrative. Chris Zeoli published on inference unbundling. Arca reframed the Kelp aftermath as a composability crisis.

1/ McKinsey Just Killed the Stablecoin Payments Narrative

[STABLECOINS]

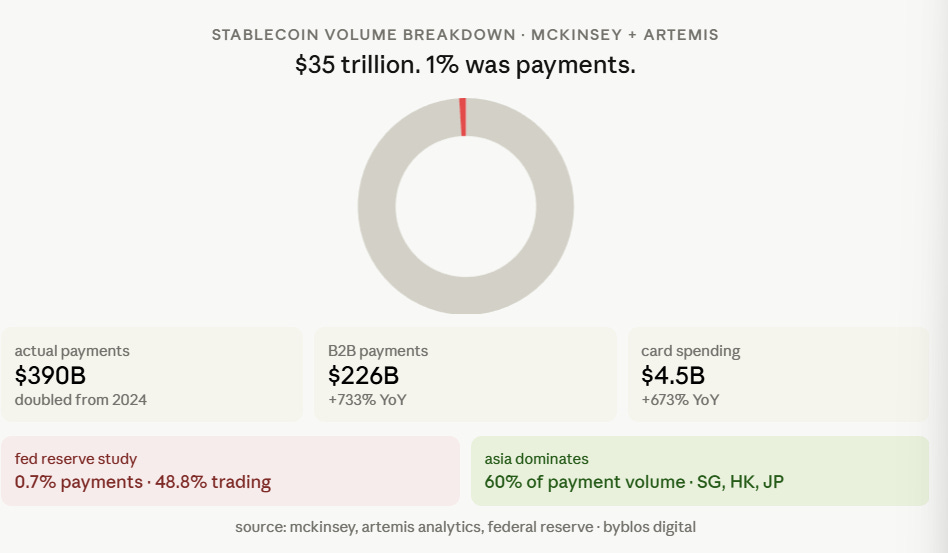

McKinsey partnered with Artemis and published what the industry was hoping nobody would dig into. Of $35T in stablecoin volume in 2025, only $390B, about 1%, was actual payments. The rest: trading, internal transfers, arbitrage, automated activity. The Federal Reserve found the same thing: 0.7% payments, 48.8% trading.

The "$33T stablecoin volume vs $25.5T credit card transactions" comparison is apples to oranges. We're comparing a settlement layer to a payment network.

But $390B in actual payments isn't nothing. It doubled from 2024. B2B dominates at $226B (up 733% YoY). Card spending hit $4.5B (up 673%). Asia is 60% of volume.

The Breakdown's framing: stablecoins aren't replacing Visa. They're replacing prime brokerage. For founders: if your deck says "replacing Visa", update it before McKinsey's data lands in your VC's inbox.

Why it matters: Settlement infrastructure, not payment network.

2/ The GPU Is Splitting in Two

[INFRA]

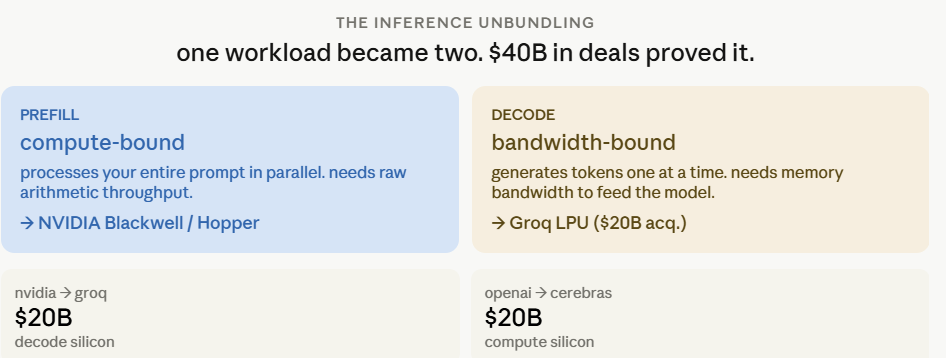

Chris Zeoli published "The Inference Unbundling" and it explains a $40B week. LLM inference has two workloads: prefill (processes your prompt, needs compute throughput) and decode (generates tokens one at a time, needs memory bandwidth).

Nvidia bought Groq for $20B to get bandwidth-optimized decode chips. OpenAI committed $20B to Cerebras for similar reasons. The single GPU doing everything era is ending. The future is routed inference stacks: different chips for different parts of the same request.

For founders: inference costs are about to restructure. Specialized silicon = cheaper tokens. The founders who understand this architecture make better infra decisions.

Why it matters: Specialized chips. Cheaper inference.

All of this was pulled from the Byblos live feed - 600+ VC firms, 27500+ newsletters, one place.

See what else came in today at byblos.digital →

3/ Composability Was the Contagion Channel

[DEFI]

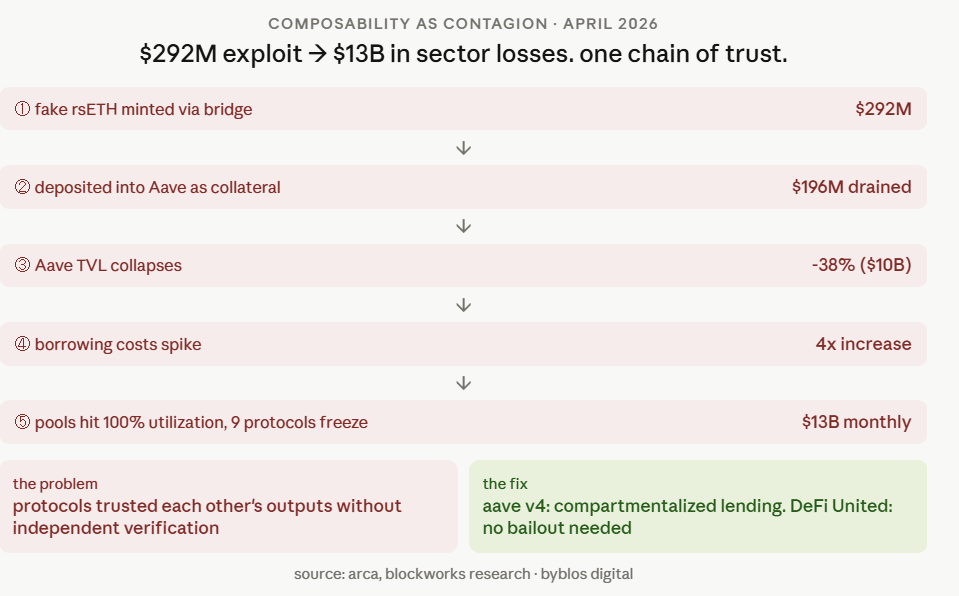

Arca's Kelp aftermath analysis reframes DeFi's core selling point. Composability, everything talks to everything, was the mechanism that turned $292M into $13B.

The chain:

fake rsETH minted → deposited into Aave as collateral → $196M drained → Aave TVL collapses 38% ($10B) → borrowing costs spike 4x → pools hit 100% utilization → nine protocols freeze.

Every step happened because protocols trusted each other's outputs without independent verification.

Compare to 2008: CDO interconnectedness spread Lehman's collapse. Nobody called interconnectedness a feature after that. Aave v4 introduces compartmentalized lending. DeFi United coordinated without a bailout, genuinely mature. But the lesson: design for isolation first, composability second.

Why it matters: Composability is a contagion channel.

4/ Perps Are Eating Every Asset Class

[DERIVATIVES]

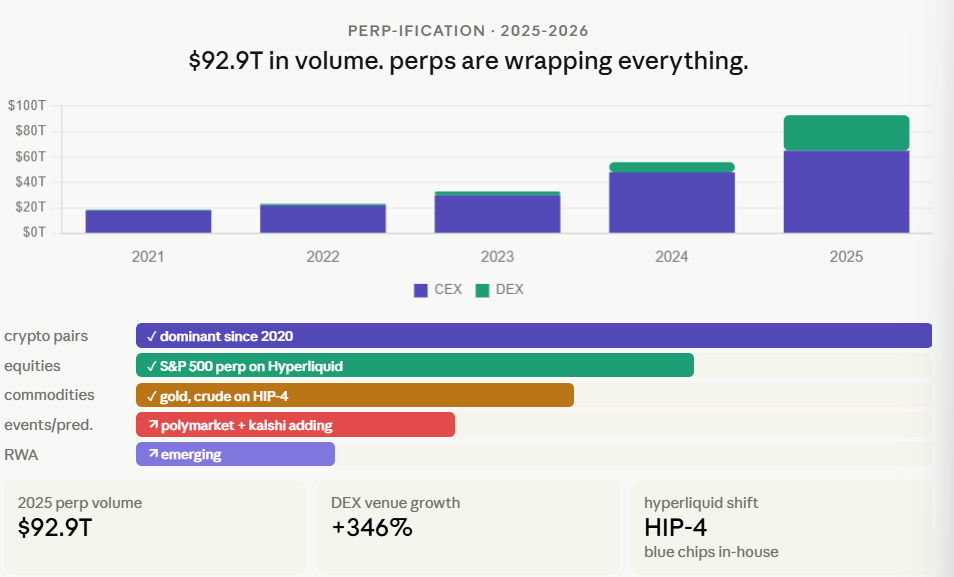

Perpetual swaps hit $92.9T in 2025 volume. Decentralized venues grew 346%. This week: Hyperliquid listed an S&P 500 perp. Polymarket and Kalshi announced perps expansion. Phoenix launched a Solana perp DEX with instant settlement and zero gas.

The pattern: perps started with crypto pairs, then equities, commodities, indices, now RWA. The perpetual swap is becoming the default derivative wrapper for everything.

Hyperliquid's HIP-4 shift is the tell: they outsourced 94% of listings to deployers, now they're pulling high-volume canonical markets (gold, S&P, crude) back in-house. Keep the blue chips, outsource the long tail.

For founders: synthetic exposure to any asset is becoming cheap and permissionless.

Why it matters: $92.9T. Perps are the default wrapper.

Today Signal Question

McKinsey says 99% of stablecoin volume isn't payments. The GPU is splitting into specialized chips. DeFi's composability turned out to be its biggest vulnerability. And perps are quietly wrapping every asset class.

Which of these changes your roadmap this week?

Everything in today’s digest came from the Byblos live feed. The full newsletter archive, the VC directory, and tomorrow’s signal are all waiting for you at Byblos.digital - the investor interned, curated.

That’s the week. Now go build something.